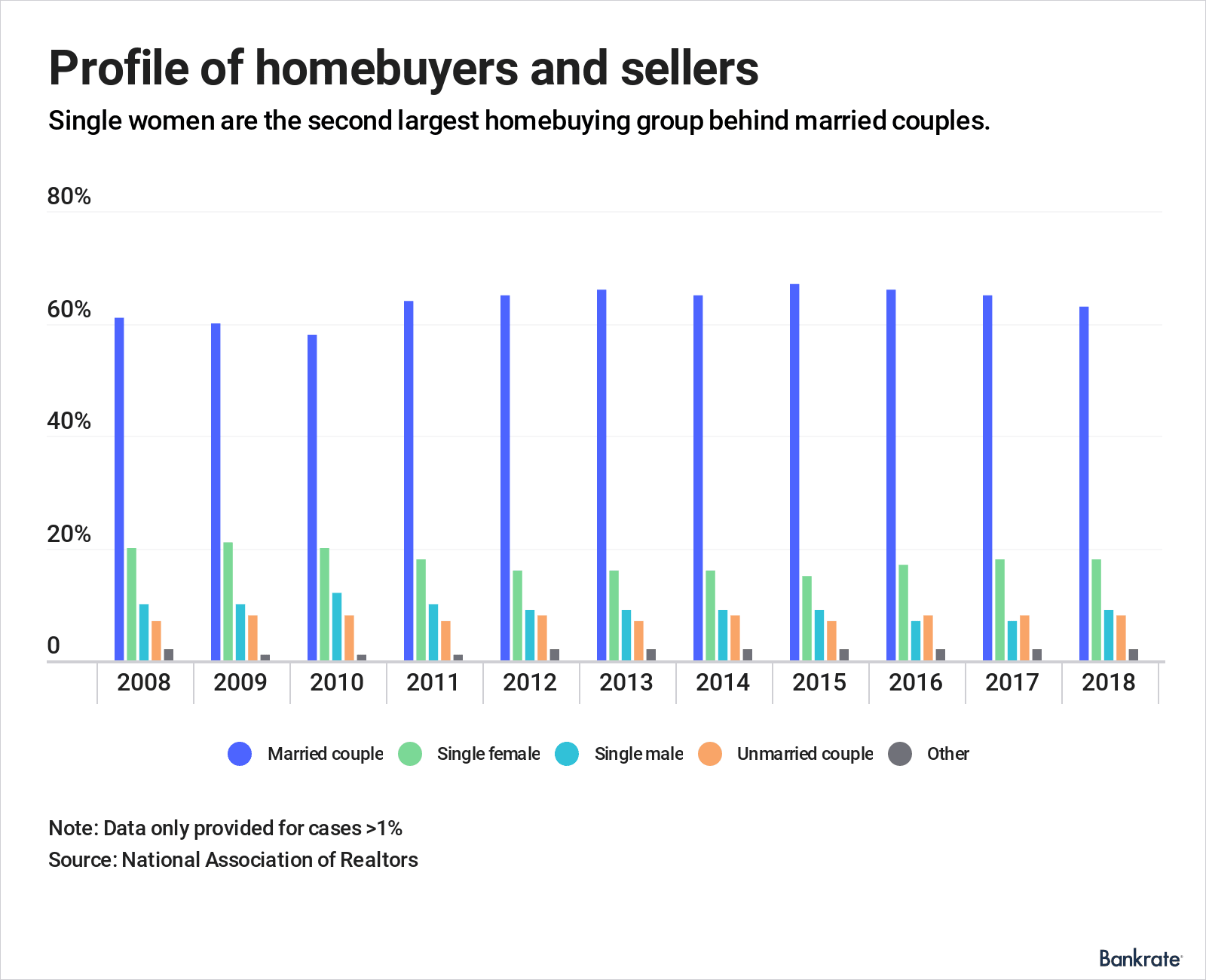

Single women are now the second-largest homebuying demographic in the United States, after married couples.

More and more women are deciding to take their futures into their own hands without waiting for a partner.

Roughly a fifth (18 percent) of all homebuyers were single women in 2018, according to the National Association of Realtors’ 2018 Profile of Home Buyers and Sellers.

But what should single female homebuyers watch out for, and how can they ensure they make the right choices? Check out the Top 7 Tips for Buying a House as a Single Woman

1. Do Your Research

Chances are, you are not taking this decision lightly, but it is still worth taking a moment to fully evaluate your choice. Buying a home when you’re single can mean freedom, independence, and the ability to go for what you want without waiting for someone else to come along. However, it is also a big, scary financial decision. The Balance recommends taking a homeownership class and familiarizing yourself with the pros and cons of your decision. A good agent is one of your best resources for making sure you’re on the right track and can help you evaluate potential homes.

2. Check Your Credit

When you buy a house by yourself, there is only one credit score being evaluated: your own. This means there is less room for error than if you were applying for a loan as a couple. However, as long as you make smart credit decisions, this shouldn’t be too much of a problem. Start by checking your credit report to see where you stand, and then start boosting it. Getting pre-approved for a mortgage is always a great first step to making sure your financial ducks are in a row and you can present a strong offer to sellers. Your lender can also provide you with tips for what to focus on and what NOT to do while you are house hunting.

3. Consider a Co-Borrower

Alternatively, you could ask someone you trust, like a parent or close friend, to be a co-borrower. Their name will be on the loan, and their income and credit history will be taken into consideration. This is an especially good idea if your credit isn’t so good. A co-borrower can either be on the title (co-applicant) or not be an owner at all (co-signer or guarantor). This comprehensive guide to co-borrowing by Better is a good place to start your research.

4. Find Helpful Programs

There are very few forms of support specifically for single women, but that doesn’t mean there isn’t any help available. Several government programs are designed to help first-time homebuyers purchase a house, whether they be single or married. Not all of them will apply to you, but it’s always worth asking your lender if you qualify.

// Buying a house when you’re single is scary, but it’s a good type of scary.

BONUS TIP!

Don’t forget to celebrate after all the stress and moving has wound down! Throw a party! Break out the bubbly! Invite all those friends and family that helped you pack and fill your new place with new memories.

Meet the Author:

Brittany Fisher spent more than 20 years as a full time Certified Public Accountant (CPA). With her extensive knowledge about taxes, personal finance and general financial literacy she runs her own site Financiallywell.info hoping to help anyone who may benefit from it.